Like clockwork each May, soon-to-be college graduates drift into New York City’s Washington Square Park in caps and gowns, typically in purple, the school colour of nearby New York University. A sea of mostly 20-somethings gather for photographs that mark the moment when the predictability of collegiate life comes to a close and new graduates face the uncertainty of what’s next.

Julie Patel, who just finished a master’s degree in public health, was one of those graduates. But a tight job market has dampened the joy of the graduation ceremony.

“I think expectations of when I came into this programme and coming out of it in terms of a job search, funding and what’s available are two very different things,” Patel told Al Jazeera.

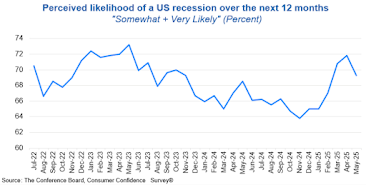

Like millions of her peers around the country, she is headed into a precarious job market amid a surge in economic uncertainty driven by a range of reasons, including tariffs, the proliferation of artificial intelligence, global conflicts and, in her case, government funding cuts in her industry, slowing hiring, especially of new graduates.

The most recent Job Openings and Labor Turnover Survey released by the United States Bureau of Labor Statistics showed that with 6.9 million open jobs in March, hirings increased marginally by 655,000 to 5.6 million, and separations were at 5.4 million. That means that for those who already have jobs, they are seldom leaving them for new ones, leaving students like Patel in a difficult position.

“The depressed hires rate suggests that it is more difficult for new entrants to get a foothold in the labour market,” Elise Gould and Joe Fast said in a recent analysis published by the economic think tank Economic Policy Institute.

“The quits rate is down, signalling a reduction in the overall churn in the labour market as workers and employers sit tight through this period of economic uncertainty, likely related to chaotic policy decisions and implementation around tariffs, deportations, and the conflict with Iran.”

The latest jobs report showed the US economy added 115,000 jobs, with most growth concentrated in healthcare, transportation and retail.

However, other white-collar sectors weakened. Financial activities lost 11,000 jobs, while information services shed 13,000. By comparison, the class of 2025 entered the job market last year when the US economy added 177,000 jobs.

Overall, job growth has slowed sharply. So far in 2026, the economy has added an average of 68,000 jobs per month, compared with 49,000 in 2025, 186,000 in 2024, and 251,000 in 2023, albeit the hefty numbers for 2023 and 2024 were on the back of layoffs during the COVID-19 pandemic.

“We have this kind of no-hire, no-fire environment right now,” Aleksandar Tomic, associate dean for strategy, innovation, and technology at Boston College, told Al Jazeera.

“We don’t see as much labour turnover as we normally would, and with the layoffs, we now have more experienced workers looking for jobs who will probably elbow out recent college graduates.”

Government funding ripple effect

Government funding cuts have hit potential employers in public health, the sector Patel is seeking work in.

Last spring, the Department of Government Efficiency – which was led by the world’s richest man, Elon Musk – slashed a myriad of government programmes and funds, which he said at the time were intended to reduce government waste. Among the cuts are roughly $4bn in funds for research awarded by the National Institutes of Health.

Cuts to research funding have led university systems across the United States to implement hiring freezes, including schools like Duke University in North Carolina and Harvard University in Massachusetts.

The universities have continued to announce cuts. Last month, the University of Maryland implemented a hiring freeze, and Princeton University cut jobs. That impacts research jobs like the ones Patel and her classmate Molly Howard are striving for.

“We’re competing not only with our cohort, but also last year’s cohort and fighting with people whose jobs have been defunded, with more experience, and everything has also been extremely difficult,” Howard told Al Jazeera.

This comes as cuts to the federal government continue. The latest jobs report showed the federal government workforce declined by 9,000 again in April – down 348,000 since a peak in October 2024- leaving those pursuing careers in public service, like Cathleen Jeanty, who is earning her master’s degree in international affairs from Columbia University, with fewer opportunities, and ramping up competition for roles at think tanks.

New graduates are also competing against students still in school for internships.

“I feel like I found myself competing for internships with people who are graduating, and then the people who are graduating are competing for jobs with people who lost their jobs due to funding cuts, the closure of USAID [US Agency for International Development], the UN’s funding cuts, et cetera,” Jeanty said.

“It kind of feels like everyone is competing with people you would assume they would not be competing with.”

AI looms

Artificial intelligence is weighing on the workforce for entry-level employees as well.

There’s a 16 percent decline in relative employment for early-career workers, including software engineers and those working in customer service-facing roles, while growth for more experienced workers remains fairly stable, according to analysis from Stanford Digital Economy Lab that examined AI-exposed sectors.

“AI is really disrupting the entry-level job market. We’re seeing evidence of that. It’s doing two things: making it more difficult for entry-level candidates, while also increasing demand for more experienced workers,” Tomic said.

That is only expected to tighten as time goes on. A Goldman Sachs survey published earlier this month found that advancements in AI translate to an average of 16,000 jobs cut from the economy each month.

Anthropic CEO Dario Amodei said several times over the last year that AI could eliminate half of entry-level jobs in white-collar sectors within the next five years.

The popularity of AI tools has tumbled among Gen Z in the last year. Twenty-two percent of Gen Z respondents are excited about AI, down 14 percent from this time last year as they enter a market with more competition across age brackets, according to a Gallup survey.

“For the first time in decades, college graduates are coming into a labour market where they are competing against their peers, millennials, Gen X, and, in some cases, baby boomers who have recently been laid off due to the uptick in AI. In many instances, entry-level roles have been eliminated and fully replaced by AI,” Stephanie Alston, CEO of BGG Enterprises, a recruitment firm, told Al Jazeera.

New graduates are also grappling with a job application process increasingly shaped by AI, making the barrier to entry even harder. AI-assisted resumes in overwhelmed applicant portals and the rise of fake applicants have strained the hiring process. The consulting firm KPMG forecasts that by 2028, one in four job applicants will not even be real.

“I have had a few interviews, but if I have to be completely honest, in the last month, I have applied to 60 roles and my response rate is about 10 to 12 percent, and it’s frustrating,” Vivica D’Souza, who recently earned a master’s degree in media innovation and data communication from Northeastern University, told Al Jazeera.

With AI now, there is also a phenomenon in which applicants are being interviewed by AI recruiters before speaking to a real person.

Courtney Gladney, who just graduated from the historically Black college (HBCU), LeMoyne-Owen College in Memphis, Tennessee, with a bachelor’s degree in business administration, told Al Jazeera that he has been in interviews conducted by AI personas.

Gladney was in the workforce before returning to school to obtain his degree.

“We’re in that age of AI. So those are new things that companies are using,” Gladney told Al Jazeera.

“I feel like sometimes it’s bad because I need the person in the interview to read me versus an algorithm.”

A new wave of an old problem

A difficult employment landscape is not a particularly new issue. In 2020, new graduates faced a stagnating job market driven by the onset of the COVID-19 pandemic. In 2008 and 2009, new graduates entered the workforce during the Great Recession.

However, Tomic argues that in 2026, the US economy tells drastically different stories for different people.

Turmoil during COVID, for example, hit the broader economy, while tariff pressures impact lower-income households more than higher-income ones. When it comes to jobs, AI’s displacement has put more pressure on less experienced roles and placed a higher premium on those who already have experience.

“The job market for experienced workers is very different from the one for those who are not experienced,” Tomic said.

“It [AI] has not affected experienced workers in the same way it has affected inexperienced workers. In fact, we’ve seen data showing that demand for experienced people has actually increased, while it has decreased for inexperienced workers, especially in jobs that are more prone to AI displacement.”

The unemployment rate among recent college graduates has surged twice over the last two decades. In June 2020, it reached 13.4 percent, slightly higher than the 12.9 percent rate for the general population during the height of the COVID-19 pandemic. It also climbed sharply in the aftermath of the Great Recession of 2008, reaching 7.1 percent in May 2010 after several years of rising unemployment. That figure, however, remained lower than the general population’s unemployment rate of 9.8 percent, according to data from the Federal Reserve Bank of New York.

It is drastically lower now, at 5.6 percent, but it is still higher than the rate for the general population at 4.2 percent.

Underemployment, on the other hand, has not fundamentally changed, standing at 41 percent among recent college graduates, compared with 43 percent this month 10 years ago and 42 percent at this time 20 years ago, according to data from the Federal Reserve Bank.

That also means this is not exactly uncharted territory for colleges and universities.

“We have to tell students that this is not the first time we’ve been here. I mean, this is a part of the economic cycle. This is a lived reality. There are highs and there are lows in the economy,” Christopher Davis, president of LeMoyne-Owen College, said.

Davis stressed that while AI and political uncertainty have presented challenges for students, a focus on soft skills, like in-person networking in the age of AI, will help students get further.

“The degree may get you an interview, but it’s the soft skills that not only land you the job, but allow you to keep the job.”

Source: Andy Hirschfeld, ALJazeera