The Conference Board Consumer Confidence Index increased by 12.3 points in May to 98.0 (1985=100), up from 85.7 in April. The Present Situation Index—based on consumers’ assessment of current business and labor market conditions—rose 4.8 points to 135.9. The Expectations Index—based on consumers’ short-term outlook for income, business, and labor market conditions—surged 17.4 points to 72.8, but remained below the threshold of 80, which typically signals a recession ahead. The cutoff date for preliminary results was May 19, 2025. About half of the responses were collected after the May 12 announcement of a pause on some tariffs on imports from China.

“Consumer confidence improved in May after five consecutive months of decline,” said Stephanie Guichard, Senior Economist, Global Indicators at The Conference Board. “The rebound was already visible before the May 12 US-China trade deal but gained momentum afterwards. The monthly improvement was largely driven by consumer expectations as all three components of the Expectations Index—business conditions, employment prospects, and future income—rose from their April lows. Consumers were less pessimistic about business conditions and job availability over the next six months and regained optimism about future income prospects. Consumers’ assessments of the present situation also improved. However, while consumers were more positive about current business conditions than last month, their appraisal of current job availability weakened for the fifth consecutive month.”

May’s rebound in confidence was broad-based across all age groups and all income groups. It was also shared across all political affiliations, with the strongest improvements among Republicans. However, on a six-month moving average basis, confidence in all age and income groups was still down due to previous monthly declines.

Write-in responses on what topics are affecting views of the economy revealed that tariffs are still on top of consumers’ minds. Notably, consumers continued to express concerns about tariffs increasing prices and having negative impacts on the economy, but some also expressed hopes that the announced and future trade deals could support economic activity. While inflation and high prices remained an important concern for consumers in May, there were also some mentions of easing inflation and lower gas prices.

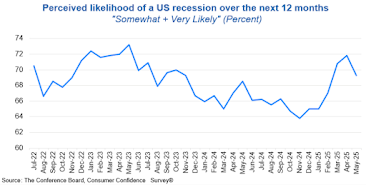

Consumers’ views of their Family’s Current and Future Financial Situations improved. The share of consumers expecting a recession over the next 12 months declined. (These measures are not included in calculating the Consumer Confidence Index®). Consumers’ expectations for interest rates ahead were little changed, while average 12-month inflation expectations eased to 6.5% after spiking at 7% in April.

Compared to April, purchasing plans for homes and cars and vacation intentions increased notably, with some significant gains after May 12. Plans to buy big-ticket items—including appliances and electronics—were also up. Likewise, consumers’ intentions to purchase more services in the months ahead, with almost all services categories rising. Dining out remained number one among spending intentions, followed by streaming services, while plans to spend on movies, theater, live entertainment, and sporting events increased the most over last month.

In a special question, consumers were asked if they changed their spending and financial behavior recently. More than a third (36.7%) said they put money aside for future spending. Around a quarter of consumers dug into their savings to pay for goods and services (26.6%) and postponed major purchases (26%). However, there were notable differences between income groups: Consumers in households making over $125K were more likely to say that they saved money while less wealthy households were more likely to have dug into their savings or postponed purchases. In addition, only 19% indicated having advanced purchases ahead of tariffs, but that share was higher for consumers in wealthier households (26%).

This month’s survey also asked consumers how worried they were about being laid off, not being able to afford necessities, and not being able to afford desired goods and services. Overall, they were more anxious about affordability than job security: Nearly half of consumers said they were concerned about not being able to buy the things they need or want, compared to less than a quarter worried about losing their jobs.

Present Situation

Consumers’ assessments of current business conditions improved in May.

21.9% of consumers said business conditions were “good,” up from 19.2% in April.

14.0% said business conditions were “bad,” down from 16.3%.

Consumers’ views of the labor market weakened in May.

31.8% of consumers said jobs were “plentiful,” up slightly from 31.2% in April.

18.6% of consumers said jobs were “hard to get,” up from 17.5%.

Expectations Six Months Hence

Consumers were less pessimistic about future business conditions in May.

19.7% of consumers expected business conditions to improve, up from 15.9% in April.

26.7% expected business conditions to worsen, down from 34.9%.

Consumers’ outlook for the labor market outlook was also less negative in May.

19.2% of consumers expected more jobs to be available, up from 13.9% in April.

26.6% anticipated fewer jobs, down from 32.4%.

Consumers’ outlook for their income prospects turned positive in May.

18.0% of consumers expected their incomes to increase, up from 15.9% in April.

13.8% expected their income to decrease, up from 17.7%.

Assessment of Family Finances and Recession Risk

Consumers’ assessments of their Family’s Current Financial Situation improved in May.

Consumers’ assessments of their Family’s Expected Financial Situation also improved.

Special Questions, May 2025

Many consumers indicated saving for future expenses, digging into their savings, and postponing major purchases…

…but there are substantial differences in behavior based on household income

Consumers are more worried about the affordability of goods and services than losing their jobs

The monthly Consumer Confidence Survey®, based on an online sample, is conducted for The Conference Board by Toluna, a technology company that delivers real-time consumer insights and market research through its innovative technology, expertise, and panel of over 36 million consumers. The cutoff date for the preliminary results was May 19.

Source: May 2025 Consumer Confidence Survey